Maize crop conditions improved following recent rainfall

South African Agricultural Commodities Weekly Wrap: 23 February 2018

February 23, 2018

Improved weather leads to increased sunflower seed plantings

February 27, 2018

Highlights in today’s morning note

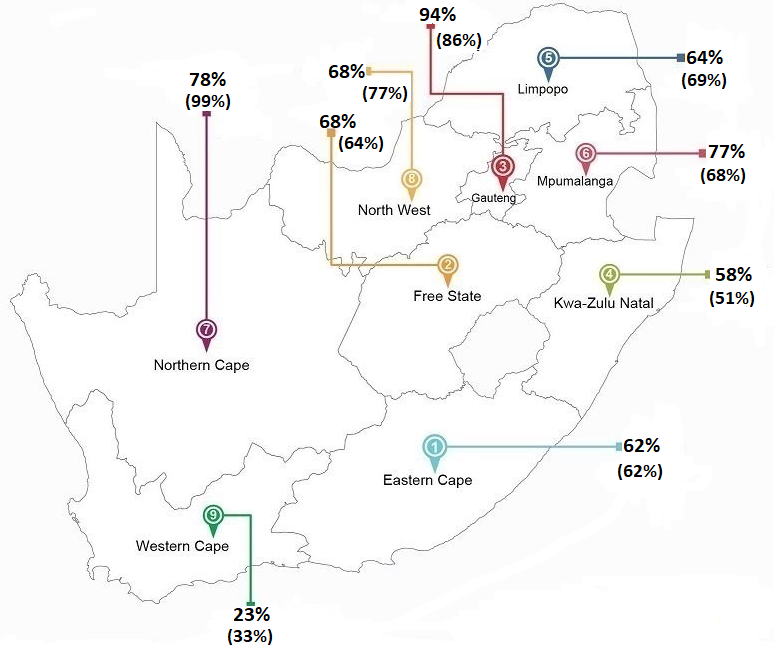

South Africa’s average dam levels: week ended 19 February 2018, with the same week last year in brackets

Source: Department of Water and Sanitation and Agbiz Research

Maize:

South Africa’s 2017/18 maize production season started on a bad footing, with extreme dryness in the western sections of the Free State and North West provinces, which led to a decline in area planted. Fortunately, crop growing conditions have since improved, following the recent rainfall across the maize belt. Moreover, the weather forecasters suggest that there is a possibility of above normal rainfall throughout the production season, which will be supportive of maize crops.

With that said, the 2017/18 maize crop could decline significantly from the previous season due to a reduction in area planted and expected lower yields in some areas. The International Grains Council recently revised its estimate for South Africa’s 2017/18 maize production down by 6% from last month to 11.8 million tonnes. This is 32% lower than the previous season’s crop.

This is not far from Agbiz’ estimate, which stands at 11.2 million tonnes, also underpinned by same reasons as the Council’s estimate. The official estimates will be released tomorrow. From a maize supply perspective, this is not much of a concern as the expected crop is well above South Africa’s annual maize consumption of 10.5 million tonnes. Moreover, there will large carryover stock of 4.2 million tonnes to boost the supplies in the 2018/19 marketing year which starts in May 2018. All of this suggests that South Africa’s maize prices could remain under pressure for some time as the market is well supplied.

Wheat:

With South Africa being a net importer of wheat, the developments in the global wheat market tend to influence local price movements. While there were fears that drier weather conditions in the southern Plains of the US could lead to a lower harvest, the International Grains Council kept its 2017/18 global wheat production estimate unchanged from last month at 757 million tonnes, which is 0.4% higher than the previous season.

The decline in wheat production in the US, Canada, Australia, Argentina and Kazakhstan has somewhat been offset by large production in the EU region, Russia, Ukraine, China and India.

Russia has recorded a largest annual increase of 17% from the 2016/17 production season to 85 million tonnes, following an uptick in area planted, as well as higher yields. Trailing Russia is India, with an annual uptick of 14% from the 2016/17 production season to 98 million tonnes, owing to higher yields.

Also worth noting is that the International Grains Council forecasts a 1% y/y uptick in 2017/18 global wheat consumption to 743 million tonnes. About 68% and 20% of this will respectively be utilised in the food and feed industries. Overall, the 2017/18 global wheat carryover stock is set to increase by 6% from the previous season to 254 million tonnes.

Soybeans:

While the area planted increased by 22% from the 2016/17 production season to 701 000 hectares, South Africa’s 2017/18 soybean production could decline by 8% y/y to 1.2 million tonnes. This is mainly on the back of expected lower yields of 1.7 tonnes per hectare, compared to an average yield of 2.3 tonnes per hectare obtained in the 2016/17 production season. The official estimates will be released by the National Crop Estimates Committee tomorrow afternoon.

Also worth noting is that the 2017/18 marketing year will end on Wednesday, but with a large carryover stock of 340 862 tonnes, which is treble the volume seen in the previous year. This will boost South Africa’s soybean supplies in the 2018/19 marketing year, which starts on 01 March 2018.

In global markets – The International Grains Council revised its 2017/18 soybean production estimate down by 2 million tonnes from last month to 347 million tonnes. This was mainly on the back of expected lower crop in Argentina, Brazil, India, Paraguay, Uruguay and Ukraine. Overall, this is 1% lower than the 2016/17 production season. Moreover, the 2017/18 soybean ending stock is estimated at 44 million tonnes, down by 4% from the 2016/17 production season.

RSA Potatoes:

After experiencing a good run in the past few days, the potatoes market pulled back in Friday’s trade session and settled in negative territory due to a large stock of 1.09 million pockets (10kg bag) at the start of the session. The price was down by 5.90% from the previous day, closing at R31.39 per pocket (10kg).

In the session, the market saw an additional increase in producer deliveries due to ongoing harvest activity in some regions of the country. This led to a 5% uptick in daily stocks to 1.14 million pockets (10kg bag).

RSA Fruit:

The fruit market had a good run in Friday’s trade session due to relatively lower stocks. The prices of apples and bananas were up by 0.23% and 8.21% from the previous day, closing at R8.73 and R6.06 per kilogram. These gains followed a 12% and 3% respective decline in apples and bananas stocks to 142 000 tonnes and 223 000 tonnes.

The oranges market has been quite volatile due to lower stocks. Friday’s session was no different, the prices were significantly up by 64.92% from the previous day and settled at R10.72 per kilogram. This was on the back of lower stocks of 19 000 tonnes, compared to levels of over 50 000 tonnes in December 2017.

Click below to read more reports by Wandile Sihlobo

Agbiz Morning Market Viewpoint on Agri-Commodities 26 February 2018

{kind=link}

{kind=link}