Agbiz Morning Market Viewpoint on Agri-Commodities: 13 February 2018

South African Agricultural Commodities Weekly Wrap

February 9, 2018

SA agricultural employment down by 8% y/y in Q4, 2017

February 14, 2018

Highlights in today’s morning note

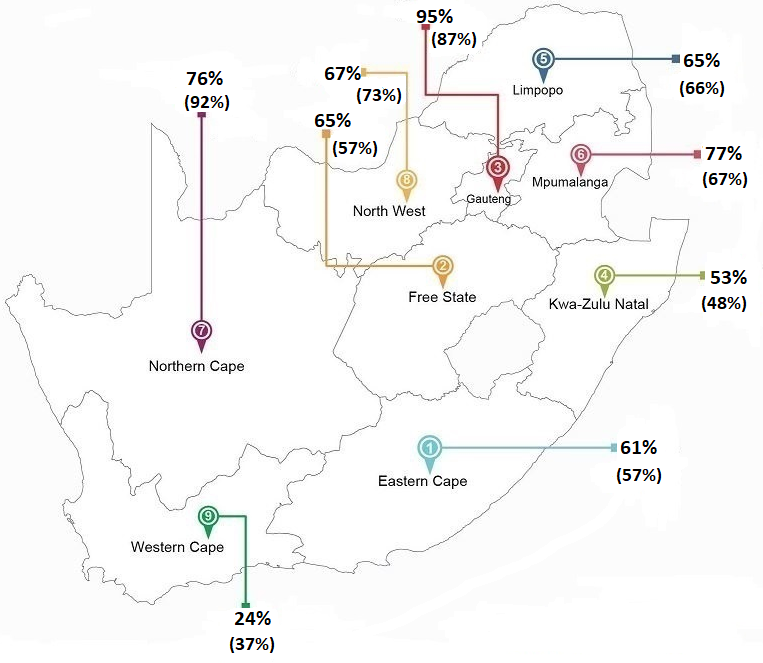

South Africa’s average dam levels: week ended 05 February 2018 (last year’s figures in brackets – 05 February 2017)

Source: Department of Water and Sanitation and Agbiz Research

Wheat:

With the winter wheat harvest process totally over in South Africa, the weather is not of importance in the market. The impact of drier conditions experienced in the Western Cape province over the past few months is mirrored in national wheat production. The 2017 harvest is estimated at 1.48 million tonnes, down by 23% y/y. This is not new news, therefore already priced into the market.

With that said, the forecast light showers of between 13 and 20 millimetres across the Western Cape province is a welcome development, although will not meaningfully improve dam levels. On 05 February 2018, the provinces dam levels averaged 24%, down by one percentage point from the previous week and 13 percentage points from the corresponding period last year.

On the global front – Recent reports from the International Grains Council shows that Egypt purchased 360 000 tonnes of milling wheat from Russia and Romania. Moreover, Iraq bought 50 000 tonnes of milling wheat from Australia. Also worth noting is that South Korea acquired 65 000 tonnes of feed wheat from the optional origin.

The USDA forecasts 2017/18 global wheat imports at 180 million tonnes, up by 1% y/y. The leading buyers, as reflected in the aforementioned recent sales, are North African countries, Middle East, as well as Southeast Asia. The Sub-Saharan Africa region is also set to be amongst the world’s wheat importing regions. Within this region, countries such as Nigeria, Sudan, Kenya, Ethiopia and South Africa are the key importers.

Maize:

This past weekend brought light showers in most parts of the South African maize belt. The western regions received rainfall varying between 07 and 50 millimetres, which mainly benefited white maize crops. Meanwhile, the eastern regions of the maize belt received rainfall of between 10 and 45 millimetres, which largely benefited yellow maize crops.

The maize crop is generally in good condition in most areas , thanks to good showers received in the past few weeks which improved soil moisture and subsequently benefited the crops . Also heartening to see is that the weather forecast for the next two weeks presents a possibility of good rainfall across the maize belt. This should further improve soil moisture and crop conditions.

Soybeans:

Bethlehem, Harrismith, Heilbron, Lindey, Vred, Warden, Bethal, Davel, Hendrina, Kriel, Eandra, Lydenburg, Middleburg, Morgenzon and Witbank regions of eastern Free State and Mpumalanga provinces received light showers of between 10 and 45 millimetres over the weekend, which bodes well for soybean crops which are already in a fair condition.

Moreover, the next two weeks could bring rainfall of between 25 and 90 millimetres across the soybean growing areas, which should further improve soil moisture, and then crop conditions. Actually, the weather forecast for the next three months is favourable, with prospects of good rainfall.

The key risk this production season is hail. In the past few weeks, hail affected few areas in KwaZulu Natal and Mpumalanga provinces, but the impact on crops was minimal, which partially explains our view of a fairly good crop this season. We forecast South Africa’s 2017/18 soybean production at 1.2 million tonnes, down by 8% from the previous season.

RSA Potatoes:

The South African potatoes market saw extended losses in yesterday’s trade session with the price down by 8% from the previous day, closing at R36.17 per pocket (10kg). These losses were partially on the back of a large stock of 1.06 million pockets (10kg bag) at the start of the trade session.

However, during the day, the market experienced commercial buying interest, coupled with relatively lower deliveries on the back of slow harvest activity during the weekend. This subsequently led to an 18% decline in daily stocks to 867 816 pockets (10kg bag).

RSA Fruit:

The fruit market ended yesterday’s trade session on a mixed footing. The price of apples was down by 13% from the previous day, settling at R8.69 per kilogram due to a large stock of 144 000 tonnes.

Meanwhile, the prices of bananas and oranges increased by 6% and 16% from the previous day, closing at R5.33 and R6.31 per kilogram, respectively. In the bananas market, the gains followed a 9% decline in daily stock to 296 000 tonnes. The oranges price was also supported by the lower stock of 7 000 compared to levels of over 30 000 tonnes at the beginning of the month.

Click below to read more reports by Wandile Sihlobo:

Agbiz Morning Market Viewpoint on Agri-Commodities 13 February 2018

{kind=link}

{kind=link}