Agbiz Morning Market Viewpoint on Agri-Commodities: 13 April 2017

Agbiz Morning Market Viewpoint on Agri-Commodities: 12 April 2017

April 12, 2017

Local innovation challenges

April 13, 2017

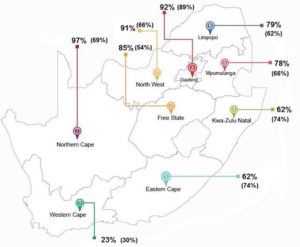

South Africa’s average dam Levels: week ended 10 April 2017 (last year’s figures in the brackets) Source: Department of Water and Sanitation and Agbiz Research.

Maize:

Maize harvest process is underway in some parts of South Africa, particularly the irrigation and the areas that planted early in the season. In the week ending 07 April 2017, total maize producer deliveries were recorded at 90 554 tonnes (57% was white maize and 43% was yellow maize). This is 27% lower than the volume delivered the previous week. The total maize producer deliveries for “week 1 to 49” currently stand at 7.1 million tonnes.

Weather forecasts show a possibility of widespread showers across the country within the next eight days. This will benefit the areas that planted late, particularly around the North West province. Moreover, dam levels could also see improvement and benefit the irrigation areas over the coming months.

On the global front, this morning Chicago maize price were up by 1.09% from the level seen at midday yesterday, owing to a weaker US Dollar against major currencies, as well as fears of planting delays due to wet weather conditions across the US Midwest.

Wheat:

The market’s attention is shifting to the planting of the 2017 winter wheat, which will commence soon. Unfortunately, the weather forecast has changed drastically from a rain promising outlook that was presented earlier this week to a drier and warm outlook for the next two weeks across the Western Cape province. This could cause planting delays in most areas that typically start early with planting activity.

More concerning is that the dam levels are at critically low, which could delay the planting activity in the irrigation areas. Data from the department of Water and Sanitation shows that in the week ending 10 April 2016, the Western Cape average dam levels were at 23% full, which is 7% lower than the corresponding period last year.

South African farmers continue to deliver wheat to commercial silos. In the week ending 07 April 2017, wheat deliveries were recorded at 3 435 tonnes, which is well below the previous week’s level of 14 804 tonnes. This brought South Africa’s 2016/17 total wheat deliveries for “week 1 to 27” to 1.85 million tonnes.

Soybean:

Soybean harvesting in underway around the eastern parts of South Africa, but not yet in full swing. So far, the yields are reportedly average to above average, which supports the National Crop estimate Committee’s view of a possible record crop. The expected rainfall within the next eight days could cause harvest delays in some areas, but still, benefit the areas that planted late.

In global markets, this morning Chicago soybean price was up by 0.95% from the level seen at midday yesterday, due to the weaker US Dollar against major currencies, as well as fears of planting delays in the US Midwest (owing to wet conditions).

With that said, there is still some bearish sentiment which emanates from expected large supplies. The USDA forecasts 2016/17 global soybean production at 345 million tonnes, up by 11% from the previous season. The key contributors to this season’s global soybean crop are the US, Brazil, Argentina, Paraguay and China.

From the demand perspective, China is set to remain a key buyer of soybeans in the global market, accounting for a share of over 60% in 2016/17 global soybean demand. The country’s 2016/17 soybean import are estimated at 88 million tonnes, up by 1% from the previous season and up by 6% from the previous season.

Trailing behind China is the EU, with 2016/17 soybean imports estimated at 14.6 million tonnes, which is 3% higher than the previous season. In addition, Mexico’s is also amongst the key buyers of soybean, with imports estimated at 4.2 million, which is 2% higher than the previous.

RSA Potatoes:

The South African potatoes market lost ground, owing to large stock levels of 998 075 kg (10 kg bags) that were seen at the start of the session. The price was down by 2% from the previous day, closing at R24.95 per bag (10kg).

However, during the session, the market saw strong buying interest, which led to a 0,3% decline in stock levels to 995 529 kg (10 kg bags).

RSA Fruit:

The Johannesburg Fresh Produce Market ended the day mixed during yesterday’s trade session. The apple market managed to claw back the previous day’s losses and closed in positive territory due to strong buying interest.

The bananas market gained ground, with the price up by 12% from the previous day and closing at R8.92 per kilogramme, also supported by strong buying interest.

Meanwhile, the oranges price lost 14% from the previous day, closing at R4.05 per kilogramme due to large stock levels of 189 420 tonnes (almost double the volume seen the previous day).

Click here to read more.

Wandile Sihlobo on how the poor will be hurt by the downgrades-it can be read here.

{kind=link}

{kind=link}