Agbiz Morning Market Viewpoint on Agri-Commodities: 16 January 2018

Agbiz Morning Market Viewpoint on Agri-Commodities: 15 January 2018

January 15, 2018

(Afrikaans) Mediaverklaring: ANC se besluit oor onteïening van grond sonder vergoeding

January 16, 2018

Highlights in today’s morning note

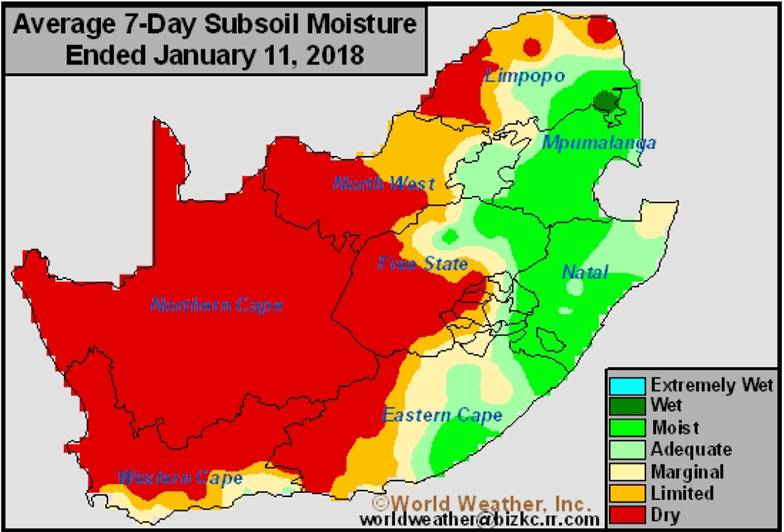

South Africa’s sub-soil moisture – 11 January 2018

Source: World Weather Inc.

Maize:

After extremely hot temperatures, some areas in the central and eastern parts of the South African maize belt received light showers last night which should improve crop conditions. Meanwhile, the western parts of the country remained dry and warm which is not good for the new season crop.

The effects of persistent dryness are clear in the western regions where soil moisture is extremely low. Thus, leading to delays in maize planting activity. Last week, farmers in the North West province had planted 70% of the intended area of 580 000 hectares. Meanwhile, farmers in the central and north-western parts of the Free State province had planted roughly 75% of their intentions.

With that said, the most recent weather forecasts for the next two weeks paint a constructive picture of rainfall across the South African maize belt. This is expected to vary between 16 and 80 millimetres and will present a much-needed relief after weeks of dryness and hot temperatures.

Wheat:

Key to monitor in the short to medium term are international wheat prices as that will have implications on domestic wheat import tariff. At the moment, the tariff rate is R716.33 per tonne, down from R910.00 per tonne in October 2017. The downward revision was linked to the higher global wheat prices.

The tariff discussion is important, as wheat imports are set to reach 1.9 million tonnes in the 2017/18 marketing year. This is double the volume imported in 2016/17 marketing year due to relatively lower domestic supplies.

The lower supplies are a function of both poor harvests, as well as relatively lower opening stock. South Africa’s wheat production is estimated at 1.48 million tonnes, which is 23% lower than the previous season due to poor yields in the Western Cape and parts of the Free State provinces. The opening stocks for the 2017/18 marketing year are estimated at 341 424 tonnes, well below the previous year’s volume of 827 232 tonnes.

Soybeans:

Although the soybean crop is generally in a fair condition relative to other crops, the extremely higher temperatures over the weekend do not bode well for the crop. With that said, there is no damage reported thus far and the weather forecasts for the next two weeks promise a widespread rainfall, which should improve soybean crop conditions across the country.

The expected rainfall is a welcome development, but hail is always a key concern for the eastern side of South Africa, especially when there are expectations of heavy rainfall. The past few weeks brought a bit of hail in some regions of Mpumalanga province, but the damage was somewhat limited. We will closely monitor the developments over the next few weeks.

Apart from this, the data calendar for this week is light, therefore, the domestic soybean price movements will largely be driven by developments in the currency market, and in Chicago soybean market.

Sunflower seed:

The expected rainfall ahead of the weekend did not materialise in the central and western parts of the country. As a result, crops that have already planted in these particular areas continue to experience heat stress owing to lower soil moisture and extremely higher temperatures.

Moreover, the time is running out for areas that have not yet planted. The optimal planting window closes around 20 January 2018, which means that South Africa will have to receive rainfall this week in order to see an increase in area planted. Farmers planned to plant 665 500 hectares of sunflower seed in the 2017/18 production season, but the key producing provinces, North West and Free State have not yet completed the process due to lower soil moisture.

Fortunately, at the time of writing, the weather forecasts were painting an optimistic picture of between 16 and 80 millimetres of rainfall in weeks between 15 and 31 January 2018. While this will not be sufficient to fully replenish soil moisture, it will be a welcome development following weeks of dryness.

RSA Potatoes:

While there was increased commercial buying in yesterday’s trade session, the potatoes market remained under pressure due to a large stock of 911 991 pockets (10kg bag) at the beginning of the trading session. The price was down by 3% from the previous day, closing at R38.47 per pocket (10kg).

During the day, the market saw strong commercial buying interest, coupled with relatively lower deliveries on the back of slow harvest activity over the weekend. This subsequently led to a 28% decline in daily stocks to 718 814 pockets (10kg bag).

RSA Fruit:

The fruit market saw widespread losses in yesterday’s trade session due to an uptick in stock levels. The price of apples was down by 3% from the previous day, closing at R8.58 per kilogram. This followed a 31% increase in daily stocks to 156 000 tonnes.

Moreover, the prices of bananas and oranges were down by 12% and 16% from the previous day, closing at R6.33 per kilogram and R4.51 per kilogram, respectively. These losses were mainly on the back of relatively large stocks of 292 000 tonnes of bananas and 25 000 tonnes of oranges.

Click below to read more reports by Wandile Sihlobo

Agbiz Morning Market Viewpoint on Agri-Commodities 16 January 2018

{kind=link}

{kind=link}